Financial Aid & Business Office Operational Alignment Services

Within higher education institutions, the Financial Aid Office and the Business Office perform distinct but closely connected roles in the administration of federal Title IV financial aid programs. Federal financial management principles require both coordination and separation of duties between these offices to maintain proper internal controls.

The Financial Aid Office is responsible for determining student eligibility, awarding aid, and ensuring compliance with federal Title IV regulations. The Business Office is responsible for institutional billing, student account management, fund posting, refunds, and financial accounting. While these functions must operate in coordination, maintaining appropriate separation between them is essential for protecting institutional integrity and federal funds.

When operational responsibilities between these departments are clearly defined and well coordinated, institutions are better positioned to maintain compliance with federal regulations, strengthen internal financial controls, and ensure that student accounts are administered accurately and efficiently.

However, in many institutions—particularly those that have grown quickly or have experienced leadership turnover—departmental roles can gradually become blurred. Over time, certain operational practices may evolve informally and become normalized without being periodically reviewed for compliance implications.

For example, during a recent consulting engagement, an institution had developed an operational practice in which the Financial Aid Office was expected to inform the Business Office what tuition amount should be charged to a student account based on the student’s financial aid package. While this workflow had evolved as a practical solution over time, it raised concerns from a compliance and internal control perspective.

Under strong internal control structures, the Business Office is responsible for establishing and applying institutional charges, while the Financial Aid Office determines eligibility and authorizes aid disbursements. When these roles overlap, auditors and compliance professionals often view the arrangement as a potential internal control weakness.

The concern is not necessarily that misconduct is occurring, but rather that the operational structure does not adequately prevent the possibility of inappropriate coordination between departments regarding student charges and aid eligibility. Federal financial management expectations emphasize systems designed to prevent such risks before they occur.

Situations like this illustrate how operational practices that develop gradually over time can unintentionally create compliance exposure, even when institutional staff are acting in good faith.

Financial Aid & Business Office Operational Alignment Services help institutions review these operational relationships, clarify departmental responsibilities, and ensure that internal processes align with both regulatory expectations and sound financial management practices.

By strengthening coordination between these two critical offices while maintaining appropriate separation of duties, institutions can improve compliance posture, enhance operational clarity for staff, and provide a smoother financial experience for students.

An operational review designed to clarify the appropriate division of responsibilities between the Financial Aid Office and the Business Office in accordance with Title IV internal control expectations.

In many institutions, operational roles evolve informally over time, which can result in overlapping responsibilities or unclear accountability between departments. This engagement evaluates whether institutional practices properly separate functions responsible for aid authorization, financial accounting, and reconciliation.

Scope:

financial aid awarding authority

student account billing responsibilities

fund disbursement coordination

reconciliation procedures.

A structured review of the operational relationship between the Financial Aid Office and the Business Office. This assessment evaluates communication processes, workflow coordination, and institutional procedures that affect Title IV compliance.

The review identifies gaps in coordination that can lead to operational inefficiencies, delayed refunds, reconciliation errors, or audit findings.

Deliverables include a written risk summary and operational improvement recommendations.

Driven by curiosity and built on purpose, this is where bold thinking meets thoughtful execution. Let’s create something meaningful together.

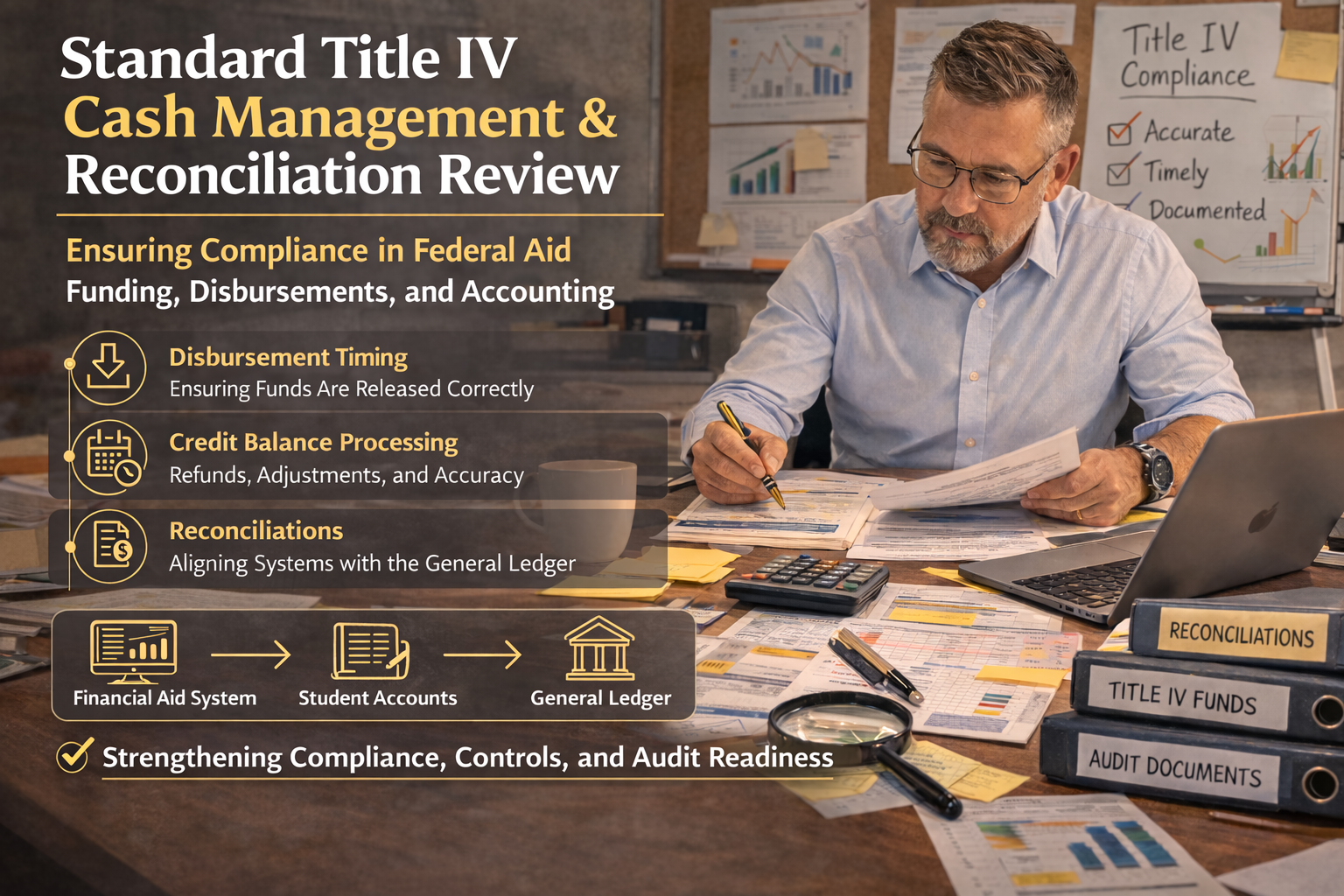

A compliance-focused review of the institution’s Title IV cash management processes under standard federal funding rules.

Scope:

Evaluation financial aid authorization

federal fund drawdowns

student account postings align with federal cash management regulations

institutional accounting practices

disbursement timing

credit balance processing

reconciliation between financial aid systems and the general ledger.